Table of Contents

A Comprehensive Guide on How to Make a Personal Savings Plan

Have you ever experienced a sense of panic and despair when you realize that you have zero savings and you’ve spent all of your money month after month? You know… the gut wrenching feeling in the pit of your stomach every time you go to check your bank account…

If you’re all to familiar with this feeling, it’s probably time to learn how to make a personal savings plan and how to manage your money better!

Whether you’re trying to stash a rainy day fund or you’re saving up for a house, car or vacation, having a savings that you can depend on can be comforting and make life less stressful. And if you’re not sure how to start, how much to save or where to secure your savings, don’t worry – I’ve got you covered!

This post may contain affiliate links. This means that we may make a commission if you make a purchase via a qualifying link (at no extra cost to you!). You can read our full disclosure for more info.

According to Market Watch, Americans are not saving as much as they used to! In fact, many persons do not even have an emergency fund to cover 3 months of expenses!

Learning how to make a personal savings plan can be as simple as deciding to save $25 and stuffing it in an envelope under your mattress. Or you can learn how to maximize your savings, benefit from interest rates with specific savings accounts, and have your finances down to a T, by making a personal savings plan!

What is a Savings Plan?

A savings plan is a system or method for how you are going to save money. Having a plan means that you have an overall picture of your finances and you know exactly how much you can save weekly or monthly.

It is a financial tool that helps you regularly set aside money in savings accounts, for investments (ETFs, funds or stocks), for sinking funds (e.g. an upcoming vacation), for retirement, for college and more!

There are several types of savings plans – personal savings plans, education savings plans, retirement savings plans, high-interest savings plans and more. Savings plans help you achieve your long-term and short-term financial goals and is a strategy every responsible adult should develop!

This post focuses on how to make a personal savings plan – that is, one that helps you save for your unofficial, personal goals. It’s a good start for beginners who are now dabbling in growing a savings account!

Why should you create a Personal Savings Plan?

“I regret having a savings account!” said no one ever!

There are so many reasons why every adult should develop a personal savings plan and grow a savings account. Seriously, a savings account is a safety net that makes adulting and adulthood so much easier! It gives you financial control, can keep you out of debt and gives you peace of mind, just to name a few.

Creating a personal savings plan is important because it helps you align your savings with your goals and ensures that you maximize your savings based on your income and expenses!

Advantages of a Making a Personal Savings Plan

• Provides a safety net for unforeseen future financial misfortunes

• Provides peace of mind

• Helps you maximize your savings based on your income and expenses

• Provides opportunities to benefit from interest or tax advantages

• Helps you achieve your goals by allocating specific amounts of money towards it

• Helps you achieve financial freedom from better money management (e.g. helps you get out of debt/keeps you out of debt)

• Helps you build financial discipline

Disadvantages of Making a Personal Savings Plan

• You’ll have less cash in hand each month for spending

• It can be a sacrifice at first as you adjust to your new lifestyle

As you can see, the benefits of making a personal savings plan far outweigh the disadvantages of not having one!

Do you need a Personal Savings Plan?

Do you need a personal savings plan like you need food and shelter for survival? No. Do you need a personal savings plan to have better control of your finances? Yes! Absolutely!

In my opinion, every responsible adult should have a personal savings plan. I mean…look at all the advantages that we just explored! Who wouldn’t love a paid-for-in-cash vacation, zero debt and a hefty emergency fund?!

But don’t worry, if you don’t know how to get started, let’s delve right in to our step by step guide on how to make a personal savings plan – complete with examples and templates! You are just a few steps away from savings success!

How to Make a Personal Savings Plan – Step by Step with Examples

1. Take a Look at your Overall Budget

Before setting up any savings plan, the first step is to take a look at your overall budget. Before you know how much you can save, you need to know how much you make and how much your expenses are each month!

Firstly, take note of your net income. This is how much you take home after all taxes and deductions. Your income should include all of the money you make from all of your money-making ventures. This includes your 9-5, side hustle and the extra $1000 you made from survey apps this month.

Next, write down all of your expenses. This includes your rent/mortgage, bills, loans, food and groceries, insurance – everything that you need to spend money on each month.

If your expenses exceed your income, we’ve got a problem. You either need to find ways to increase your income or cut costs and lower your expenses. Our guide on creating a budget plan explains all the details on how to do this – which is a necessary first step before creating your personal savings plan!

You see, saving money is impossible if there’s none left over to save after paying your bills. And if this is your situation after writing down all of your net income and expenses, it’s time to move on to step 2.

2. Find Ways to Cut Costs

After evaluating your expenses, are there not any apps, bills or subscriptions that can be cut? When was the last time you used your online book subscription? Do you really need THREE streaming services? Do you order often enough to justify needing a subscription for faster, next-day shipping?

If you’re not sure what services and subscriptions you even pay for at this point, it’s time to sit with your banking statements for the last few months and go through each payment with a fine-tooth comb.

Use different color highlighters to sort payments into those you knew you were paying and those you had no clue about. Trust me, it happens. I can’t tell you how many free trials I signed up for and continued paying for months (facepalm)!

If you’d prefer to have the experts look over your finances to identify and cancel unnecessary payments and subscriptions, using an app like Rocket Money is a must!

Millions of money savvy people already use Rocket Money to track finances, stay on top of bills, manage subscriptions and save money! In fact, Rocket Money boasts that they have saved their members over $1 billion and counting!

With Rocket Money, all the more money to stash into my savings account! So why don’t you cut costs and start saving with Rocket Money today?

Apart from forgotten subscriptions and unused services, you can also cut costs on food and groceries by meal planning, cooking budget recipes at home and utilizing cheap meal plans. Food is one of the most flexible aspects of our budget, so unlike the other fixed categories (like rent), how much we spend is in our control!

Simple daily money-saving habits can cut costs by hundreds of dollars – all of which can go towards your savings when you create your personal savings plan! Practicing simple frugal habits, cutting costs on the electric bill or calling companies and asking to downgrade a service for a lower payment can all add up in the end!

3. Determine How Much to Save

Once you’ve figured out how much you’re cutting on expenses, you can decide on how much money you want to save. The amount you choose to save should align with your goals and how much time you have to achieve them.

For example, let’s say you want to travel to Finland to see the northern lights during the Christmas period next year. And after your research, you’ve calculated the total cost to be $15 000 for your entire family. Now, suppose you have 16 months until November of next year (you want everything to be paid for by the month before the trip), then you can calculate a savings of $15 000 ÷ 16 = $937.50 each month.

This is called a sinking fund! A sinking fund is a savings fund where you contribute a specific amount of money each month for a future expense. You can have several sinking fund categories at a time:

• Emergency Fund – e.g. $750 per month for 12 months to cover a $9000 emergency fund (for 3 months of expenses)

Note that building your emergency fund should be your priority before adding to other sinking funds. You can either choose to save simultaneously, with the biggest portion of your savings contributing to your emergency fund or save your emergency fund first and then focus on saving for other fun goals!

• Vacation – e.g. $937.50 per month for 16 months to cover your $15 000 Finland trip

• House Maintenance – e.g. $750 per month for 12 months to cover a $9000 kitchen renovation

• Christmas – e.g. $83.33 per month for 12 months to cover a $1000 budget for Christmas presents

• Birthday Party – $200 per month for 14 months to cover a $2800 birthday party for your child

Other sinking funds may include pets, taxes, clothing, insurance, wedding, self care and more! Once it’s a goal with a price tag attached, you can create a sinking fund for it!

Obviously, your goals need to align with how much money you have at your disposal. There’s no way you can save for Finland, house maintenance and a birthday party if you only have $200 left over after your expenses. You’d either need to lower your goals and expectations (or increase your income!).

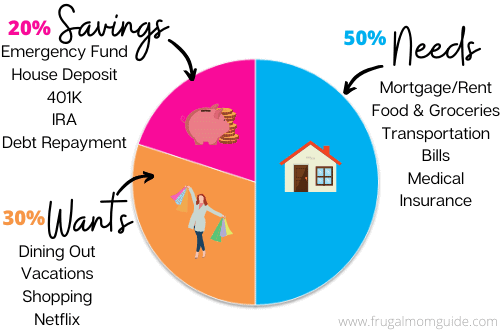

If sinking funds are not your jam, and you just want to save money each month but you’re not sure where to start or how much to save, you should check out the 50 30 20 budget plan!

This budgeting strategy encourages you to view your net income as a pie. This is your take home salary after your taxes, pensions and direct deductions have been made. Whether this pie is the pie you wanted, the size you wanted, if it’s topped with whipped cream or not, it’s the pie you have.

The rule is that 50% of this pie would be used for survival, 30% for recreational purposes and 20% saved for the future. Basically…50% must be allocated to NEEDS, 30% to WANTS and 20% to SAVINGS!

Using this strategy takes the guesswork out of how much you should be saving each month. Simply multiply your net income by 0.2 and voila! This is the amount that should be saved!

So, if you make $2350.00 per month after deductions, $470.00 (0.2 x $2 350) should go towards savings every single month.

How much you decide to save each month is up to you. You can save as little or as much as you want to!

4. Decide Where you Want to Stash your Savings

The next step is to decide where you will be stashing your savings. Your options are:

• Envelopes at Home

This method is convenient and accessible but not exactly safe. You will not be able to benefit from interests but there are also no bank fees. This is better for short-term goals with very minimal cash.

• High-yield Savings Account (HYSA)

This type of account pays a higher interest rate that a regular savings account, which means you will end up with more than you put in. HYSAs usually have an annual percentage yield (APY) of around 4% and over, allowing you to enjoy the benefit of compound interest on both the principal and the interest that the principal earns.

Long story short, you’ll get to earn higher interests on your savings, which gets added to the savings amount, which now earns even higher interests, so your funds grow faster! HYSAs are also accessible since you can withdraw at any time and may even be given a debit card (with a limited number of transactions) for convenience.

Additionally, a HYSA is usually insured for up to $250 000, giving you peace of mind that there is little to no risk involved. A HYSA is a great option when saving for your dream vacation, a wedding, a house maintenance fund or a down payment for a house or car. It is perfect for short-term goals that require saving for 3 – 24 months.

• Certificate of Deposit (CD)

If you’re absolutely certain that you wouldn’t need access to your savings (usually because you already have a separate emergency fund), you can take advantage of a CD. CDs are savings accounts with a fixed interest and a fixed period (or term).

CDs also have the benefit of higher interest rates, compounded interest and insurance for up to $250 000. However, it is expected that you keep your savings in the account for the fixed term (usually 1 month to 10 years) until it reaches maturity, otherwise you will face early withdrawal fees and penalties!

This type of savings account is perfect for short-term goals such as vacations and down payments but is not ideal if you will need access to the funds before it reaches maturity (at the end of the fixed term).

• Regular Savings Account

A regular savings account is a place to safely park your funds for easy access and a decent interest. This is a great option for saving for very short-term goals where interest is not that important. It is also usually insured and easy to open.

• Money Market Account (MMA)

MMAs usually have higher interest rates and APYs than regular savings accounts and is a great option when saving for short-term goals. It also has insurance protection and has check-writing privileges. However, there is usually a limited number of withdrawals that can be made per month and there may be minimum balance requirements.

Note that, long-term savings goals can utilize specific savings accounts such Roth IRAs or Traditional IRAs for retirement savings. This guide on how to make a personal savings plan assumes that you already have retirement savings accounted for and your current personal savings plan is separate from your long-term 401(k) contributions.

5. Increase your Income

If you don’t have enough to save for a Finland vacay or to throw a surprise party for your kid, your only option is to increase your income. If you’re trying to find quick and easy ways to make money from your phone, you might want to try an app like Swagbucks to get paid for completing simple tasks online.

Or if you’re really struggling, you can take advantage of same day pay jobs for access to extra cash straight away! Imagine growing a side hustle that can finance all of your sinking funds and afford you a luxurious lifestyle!

If you’re introverted like me, and don’t mind waiting a while for your side hustle to become profitable, you could start a blog (like this one). Believe it or not, this blog makes me 6-figures and way surpassed my 9-5 income! Learn exactly what I did to get started!

All in all, increasing your income is an important part of creating your personal savings plan. Because the more you make, the more you can save!

6. Keep on Track & Stay Motivated with a Saving Money Plan Template

Once you’ve figured out how much you want to save each month (maximizing savings by cutting costs and increasing income) and where you want to stash your savings, stay motivated and keep track with savings trackers and templates.

You can create your own fun printables or you can use ours to set you up for success! Why not grab our Budget Printable Pack to get started? It’s totally free!

Personal Savings Plan Examples

Now that we understand how to make a personal savings plan, let’s look at some actual examples!

Example 1 (How to Make a Savings Plan using Sinking Funds)

Lets say that Jane’s annual take home salary is $60 000.

Jane’s Net Monthly Income:

$60 000 ÷ 12 = $5 000

Jane’s Total Expenses:

Mortgage $2 547

Vehicle Payment $521

Gas $150

Food & Groceries $550

Internet $78

Streaming Service Subscription $15

Utility Bills $225

Loans & Credit Card (Minimums) $370

Total expenses = $4 456

Amount Leftover after expenses: $5 000 – $4 456 = $544

This is the amount that Jane has leftover for saving after all expenses are paid. If Jane wants to save more money, Jane will now evaluate where she can cut costs (e.g. saving $50 on groceries by skipping takeout and cooking all meals all month & saving $15 extra by cutting her streaming service indefinitely).

Jane can also decide to work overtime or start a side hustle to have more money at her disposal – some or all of which can go towards her savings.

Alternatively, Jane can decide that she’s okay saving less than $544 and wants to allocate $100 of that to fun and recreation each month. It’s really all up to Jane and how fast she wants to achieve her goals!

Let’s say Jane is fine with saving $544 each month and she already has an emergency fund. It’s time to align her saving with her goals.

Jane’s Goals:

• Vacation to Finland in 36 months

• Birthday party for her kid in 12 months

The cost of the Finland trip for her family is $15 000. Over a 24 month period, this will amount to payments of around $417 ($15 000 ÷ 24) each month.

The cost of the birthday party is $1 000. Over a 12 month period, this will amount to payments of around $84 ($1 000 ÷ 12) each month.

• Finland Vacation Sinking Fund = $417 per month

• Birthday Party Sinking Fund = $84 per month

Total Savings = $501

Now Jane has $544 – $501 = $43 remaining. Jane may choose to save this by adding it to a separate “Miscellaneous Sinking Fund”, or she can put it towards the principal on her current loans/debts, or she can add it to her fun and recreation category.

Finally, Jane will decide where she wants to save her money. She may decide to add her Vacation Savings to her high-yield savings account at her local bank. However, she will add $84 each month to an envelope hidden inside her favorite novel, to cover the cost of the birthday party.

This is a detailed look at Jane’s Personal Savings Plan!

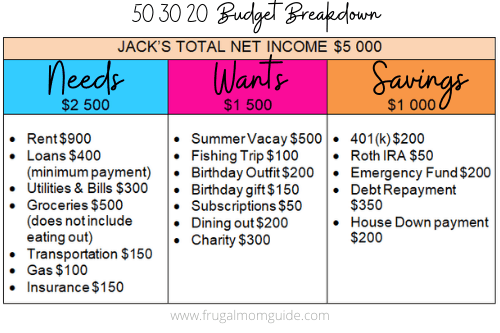

Example 2 (How to Make a Personal Savings Plan using the 50 30 20 Budget Rule)

Let’s say John’s annual take home salary is $30 000 per year. Let’s work out a 50 30 20 budget for him.

John’s Monthly Income: $30 000 ÷ 12 = $2 500

Amount for Needs: 0.5 × 2 500 = $1 250

Amount for Wants: 0.3 × 2 500 = $ 750

Amount for Savings: 0.2 × 2 500 = $500

John has decided that he will stash $500 into a regular savings account every single month! His goals are to travel to Finland ($15 000) in 36 months. By then he will have saved $18 000 and will withdraw for his vacation from this.

The leftover $3 000 in savings will remain in his account as he currently has no other short-term financial goals. He is already spending $750 on “wants” each month so John is pretty satisfied and contented with life.

Whichever method you choose is totally up to you, your finances, your preferences and your lifestyle! Either of these strategies will help and encourage you to keep saving and maintaining control over your financial life.

5 Savings Accounts with the Best Return

We’ve already looked at the various types of savings accounts and the pros and cons of each. Here, we’ve simply listed and ranked these savings accounts according to highest returns.

Feel free to go to your local bank to discuss specific rates or even check out and sign up with a virtual bank for even higher interest rates!

1. Money Market Account – highest interest rates (4%+), limited number of withdrawals per month

2. Certificate of Deposit – highest interest rates (4%+), penalties for early withdrawal, funds should be left until maturity

3. High-Yield Savings Account – highest interest rates (4%+), funds are accessible

4. Regular Savings Account – moderate interest rates, funds are accessible

5. Envelopes at Home – cannot benefit from interest rates

How to Open a Savings Account

A regular savings account is the easiest to open, with the fewest hoops to jump through. However, the following is usually the procedure for opening any type of bank account.

1. Choose the type of savings account

2. Provide the required documents (such as ID, SSN, proof of address and contact information)

3. Complete the application form

4. Provide your first deposit

Additional Info on How to Make a Personal Savings Plan – FAQs

What is a personalized saving strategy?

A personalized saving strategy is a personal savings plan that is customized to an individual’s income, expenses, lifestyle and goals. It is tailored to help this particular person achieve their goals within their preferred timeline.

What is the 50 30 20 rule of money?

The 50 30 20 rule of money is a budget plan that specifies how you should spend your net income. According to this rule, 50% of your net income should be allocated to needs (rent, minimum payment on loans, bills, transportation, insurance etc.), 30% should be allocated to wants (clothes, self care, dining out etc.) and 20% should be allocated towards savings (emergency fund, house down payment etc.).

How to save $10K in in 3 months?

To save $10 000 in 3 months, you’d need to be saving around $3 333 per month or $833 per week! Most people don’t just have this kind of cash lying around to stash into savings so the key to doing this is developing a high-paying side hustle or two. The more you make, the more you can save!

It’s not impossible. After all, we we able to save $24 000 in just 7 months (quite recently!) when we were saving for a house down payment. The trick is to side hustle and then side hustle some more!

Related Posts on How to Make a Personal Savings Plan

7 Little Habits to Skyrocket your Savings Immediately

29 Best Money Saving Apps to Turbo-Charge your Savings Account

Final Thoughts on How to Make a Personal Savings Plan

When you learn how to make a personal savings plan and actually follow through with it, so many financial benefits come along with it – achieving dream goals without going into debt, peace of mind from being in control of your finances and feeling like you rock at adulting!

Seriously, every adult should take the time to strategize and create their own personalized savings plan. And if you haven’t done so already, what are you waiting for?

Do you have any other tips or questions about making a personal savings plan? Share with us in the comments below. We’d love to hear from you!

Be sure to follow us on Pinterest, Instagram and Facebook for more money saving hacks and tips to making the most of your money. All while enjoying life to the max!

Liked this post? Pin it!

Leave a Reply